We recently shared this market update as part of our 4Q2023 update to our own investors. We’d like to share this context more broadly as it may be helpful to founders, LPs, VCs, and others elsewhere.

After a difficult year for the industry, 2023 ended on a strong note with a lot of positive momentum going into the new year. Public markets had a strong quarter, with the cumulative market cap of crypto assets increasing by 50%. It’s still too early to tell whether we are in the early innings of a bull market, but the positive price action has certainly restored some confidence across the industry and interest amongst outsiders.

This quarter also brought about the long anticipated, and ultimately widely successful, token launches of some notable projects including the likes of Celestia and Jito. If the public market continues on its current trajectory, we can expect more teams to take advantage of the opportunity to launch their tokens over the course of 2024.

On the regulatory front, after a US court’s ruling last quarter opened the door for the launch of a Bitcoin spot ETF, the anticipation of an imminent launch built up throughout the quarter (spoiler alert: the first Bitcoin spot ETF was launched at the beginning of January 2024). Most importantly, there continues to be unabated progress and enthusiasm at the earliest stage amongst entrepreneurs. A positive constant this year has been the continued technological and product development across all layers in the stack. Advances in infrastructure have steadily lowered the cost and complexity for developers to build compelling products, while at the application layer entrepreneurs continue to push the boundaries of what’s possible with crypto technologies.

We have incredible respect for all the teams that stuck to their convictions and stood up to the many challenges that came their way in 2023. Building companies is never easy and it’s difficult to imagine a more challenging environment than crypto in 2023. Yet difficult times create strong characters and we deeply believe that this past year has moulded many of the future leaders of our industry.

Public Markets

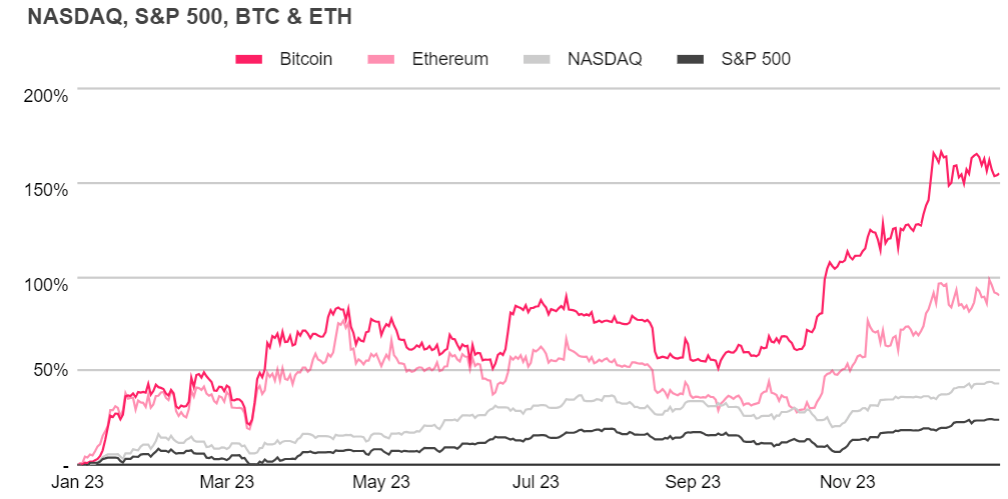

Public markets came roaring back and had their strongest quarter of the year. Large caps Bitcoin and Ethereum saw significant price surges of 51.1% and 31.6% respectively. Bitcoin ended the year up 155% from its starting price at the beginning of the year, while Ethereum was up 92%.

It’s always very difficult to attribute shorter term price movements in crypto to a particular catalyst. However, recent positive regulatory developments in the US and the expectation of the imminent launch of the Bitcoin spot ETF contributed to increased optimism and confidence in the industry.

This quarter also saw a series of successful token launches that were buoyed by the strong public markets. The most notable was arguably the launch of Celestia’s native token, TIA, which launched at the beginning of November and experienced a 457% price increase by year end. For the majority of 2023, teams held off on launching their token given how weak public markets were. As is the case when companies IPO their equity, the timing of the launch of a crypto network’s token matters. If strong public market performance and sentiment persists, our expectation is to see a lot more token launches throughout 2024.

While as long term investors we are less beholden to or interested in the short term price actions of the public markets, they remain an important tool to measure the confidence level in the industry and come with second order effects. One of these second order effects as alluded to as above is the opening of a token launch window. Additionally, if the price action continues, we expect to see rising valuations reflected in the private stage markets as well. As a whole, when public market prices rise, more investors return and push more capital into the industry.

Solana’s resurgence

Solana came into 2023 beaten and battered but at least still alive. 2022 was a tumultuous year where the network saw its TVL drop from $6.5bn to $200m, a dozen notable outages each lasting longer than half a day due to growing technical challenges, and the loss of its largest proponent and liquidity provider in FTX and Alameda Research.

Although the network’s value diminished, its core group of developers who had braved past its tough technical onboarding stuck around and kept building. Months of work were required to restabilize the ecosystem and rebuild alternatives to critical services no longer provided by FTX. The network experienced only one major outage in February and saw line of sight to further resilience with a second major client, Jump’s Firedancer, on testnet. TVL hovered between the $250-300m range until exploding to $1.5bn between November and December after a flurry of new token launches. Solana’s token price has recovered with a similar explosiveness.

All told, Solana is an incredible comeback story of an ecosystem who stuck to their convictions and faced adversity head on. Many loud voices were calling 2022 the end for Solana but the founders and teams building within the network stood by their belief in both the network’s resilience and their own products.

L2 maturity and proliferation

We have spoken on the emergence of layer 2s (L2s) a variety of times here in past quarterly commentaries, whether it be on their technological underpinnings or adoption metrics.

Coming into 2024, we view L2s as having advanced from the research and innovation phase to an instalment phase where every founder and builder is now able to cheaply launch their own blockchain as an L2. The number of L2s live or announced has exploded from just a handful at the beginning of 2023 with the large majority announced over the last quarter. We are very likely in the early innings of a “Cambrian explosion” of L2s that will play out over several years.

For projects, the customizability of an L2 enables designs towards specific use cases or user groups that would otherwise be difficult to achieve on shared environments like Ethereum or Solana. Projects can adjust fee models or enforce economic rules, such as allowing fees to be paid in a native token, sharing fee revenue with developers or smart contracts (eg. Kinto or Canto), upholding creator royalty rights for NFTs (eg. Frame or Rari), providing pass-through native yield for assets held (eg. Blast or Mode), and etc. They are also able to enforce authentication or KYC ahead of granting read or write access (eg. Kinto continuously runs KYC on all accounts).

This “now” moment stems from the maturation of the four oldest companies developing L2 technology (circa 2019, both optimistic and zero knowledge based roll-ups): Optimism, Arbitrum (Offchain Labs), ZkSync (Matter Labs), and Polygon. Beginning with Optimism in February and followed by each L2 vendor in the succeeding months, all four have now delivered production-ready, open source SDKs for developers to launch their own L2s: OP Stack (Optimism), Nitro (Arbitrum), ZK Stack (ZkSync), and Chain Development Kit (CDK; Polygon). Over 2023, each vendor has strategically transitioned from championing a single canonical instance of their L2 to becoming a technology provider to third parties through revenue share or similar partnership agreements.

The quarter in 3 charts

Public crypto markets finished the year strongly

Public markets had their strongest quarter of the year, with large cap projects like Bitcoin and Ethereum outperforming the major stock indices.

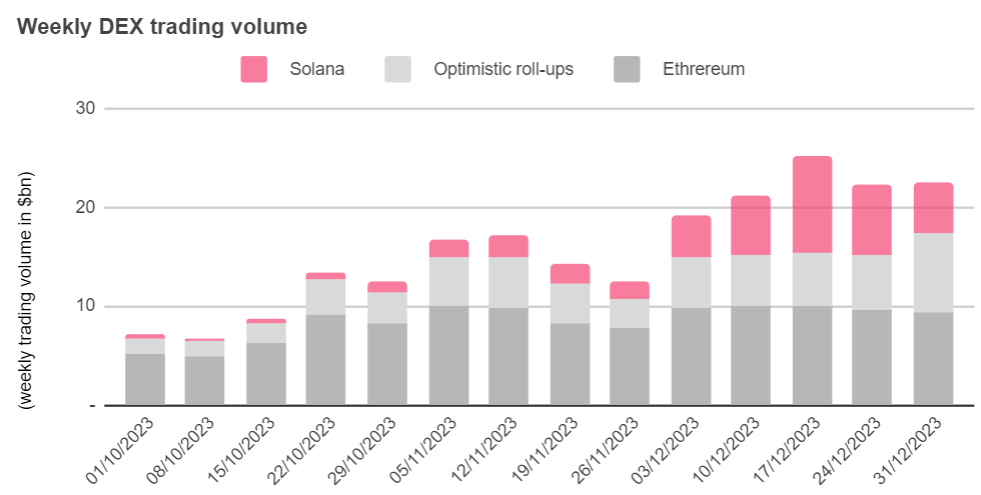

DEX trading volume picked up across chains

Trading activity experienced a significant uptick with volumes tripling over the quarter. The growth was primarily driven by Solana and optimistic roll-ups along with nearly a doubling in Ethereum’s own trading volume.

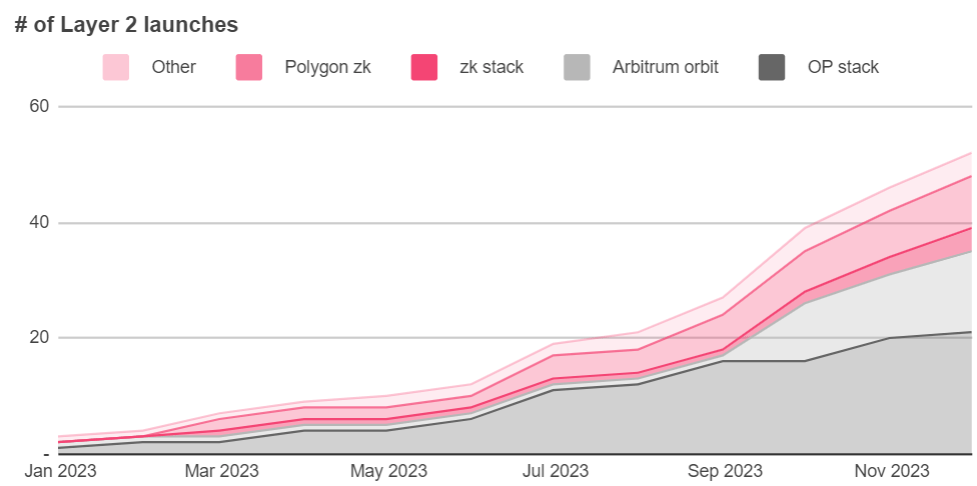

Projects launching their own L2s

We saw substantial momentum behind layer 2 (L2) launches in the last quarter of 2023, driven by leading platforms such as Arbitrum and Optimism releasing production-ready SDKs.