We recently shared this market update as part of our 2Q2023 update to our own investors. We’d like to share this context more broadly as it may be helpful to founders, LPs, VCs, and others elsewhere.

If there was one tagline we’d pick to sum up the quarter, it would be to “keep calm and carry on.” In contrast to some of the higher tenor periods in recent history, this quarter was comparatively calm.

Yes, on the regulatory side, pressures in the US continued to mount as the SEC brought suits against Coinbase and a host of other companies. Yet, this came as no surprise given the SEC’s past posturing and will no doubt mark a pivotal turning point in the industry’s continued maturation and institutional acceptance. While no legal battle is enviable, the case against Coinbase presents an opportunity for one of the industry’s leading companies to defend both itself and the broader industry against an overreaching regulator in the highest of stakes.

Furthermore, the industry continued to show its resilience. June saw Blackrock, the world’s largest asset manager, becoming the latest institution to file for a Bitcoin spot ETF. Year to date, the volume of real world assets—treasury bills, money markets funds, high-yield corporate bonds, etc—ported onto blockchains has come from near zero to the hundreds of millions. The field of decentralised science (DeSci), which is an application of web3 technologies onto the sciences, materialised early signs of its potential to improve the industry and accelerate the rate of scientific discovery.

Someone recently remarked that “crypto doesn’t seem to die.” That’s the whole point of decentralised systems, akin to the original vision of the Internet. They are much more resilient than centralised systems because they aren’t reliant on a central authority and can be upheld by many individual actors.

Politics and crypto

The SEC continued its crackdown on crypto as it followed up on the Well’s Notice issued to Coinbase last quarter and officially filed a suit. In our last update we talked at length about the regulatory climate in the US and the absurdity of the SEC going after a company whose IPO it approved 2 years ago so we’ll keep it short this time.

The reality remains the same—the US has become a hostile place for the crypto industry while other regions are trying to assert themselves. One of the most notable moves this past quarter was a16z, one of the largest investors in the space, announcing the opening of its first international office in London and plans to host the next edition of its crypto school there. The move had the support from British PM Rishi Sunak, and is the latest sign that the UK seems to be serious about its support for crypto. Elsewhere in the world, April saw the EU formally adopting MiCA and June saw Hong Kong opening their licensing program for retail-targeting crypto exchanges.

RWA

One of the themes we’ve been really excited about since the fund’s inception is the porting of real world assets (RWA) on-chain. Blockchains are great rails for value transfer not only for native assets, like BTC and ETH, but also for more traditional ones like treasury bills, money markets funds, or physical collectibles.

As rates across DeFi money markets like Compound and Aave have fallen, crypto holders have been on the lookout for alternative sources of yield. The last year has seen treasury yields overtaking DeFi-native rates, heightening the demand from crypto holders to gain exposure to treasury-denominated assets without needing to offramp their crypto. As a result, over the past few months we’ve seen an accelerating volume of treasuries and other securities like money markets funds being bridged from the off-chain to the on-chain world.

However, it’s not only existing securities that can be bridged on-chain. For example, physical collectibles like watches or sneakers can be tokenised as well. Once tokenised as NFTs, physical collectibles not only become easier and cheaper to transact with but also gain access to a rich set of features across DeFi applications. Just recently, an NFT backed by a Patek Philipe was used as collateral to take out a $35,000 loan.

The most widely adopted RWA in crypto today is the USDC stablecoin, which is backed 1:1 by dollar deposits. There’s $27B worth of USDC in circulation today. It has become an important part of the crypto industry and we think the first of many RWAs that will gain meaningful adoption.

As crypto infrastructure continues to mature and enable new applications, we believe the merging of off-chain and on-chain worlds will be an area rich with new applications yet to be built. It is an area we are looking at very closely.

DeSci

Another area we’ve been actively investing in that has begun seeing strong progress is decentralised science (DeSci), which aims to apply web3 technologies to the sciences. We previously wrote about the premise of DeSci here and its emerging technology stack here.

A lot of the interesting developments in the DeSci space right now stem from Molecule. Molecule, a company we invested in last year, is a marketplace for bio IP. Its aim is to make bio IP more liquid and easily transferable, pioneering the attachment of IP onto an NFT (called an IP- NFT) which then allows the purchasing of IP to be as easy as buying an NFT on Opensea.

In addition to the marketplace, Molecule has played an active role in seeding the first set of buyers, Bio DAOs. Bio DAOs are vertically integrated DAOs that invest in and develop IP across a variety of niche scientific fields. The number of Bio DAOs continues to grow with some examples including VitaDao for longevity, HairDAO for hair loss and AthenaDAO for women’s health.

Most recently, VitaDAO fractionalised one of its individual IP-NFTs to allow external investors to purchase a percentage of that IP-NFT’s shares. This is the first time that individuals can directly own and govern IP with small sums of capital. We think that’s important because the creation of liquid and efficient markets promises to tackle a lot of the issues in the funding of bio IP, which if solved, can speed up the rate of scientific progress.

The quarter in 3 charts

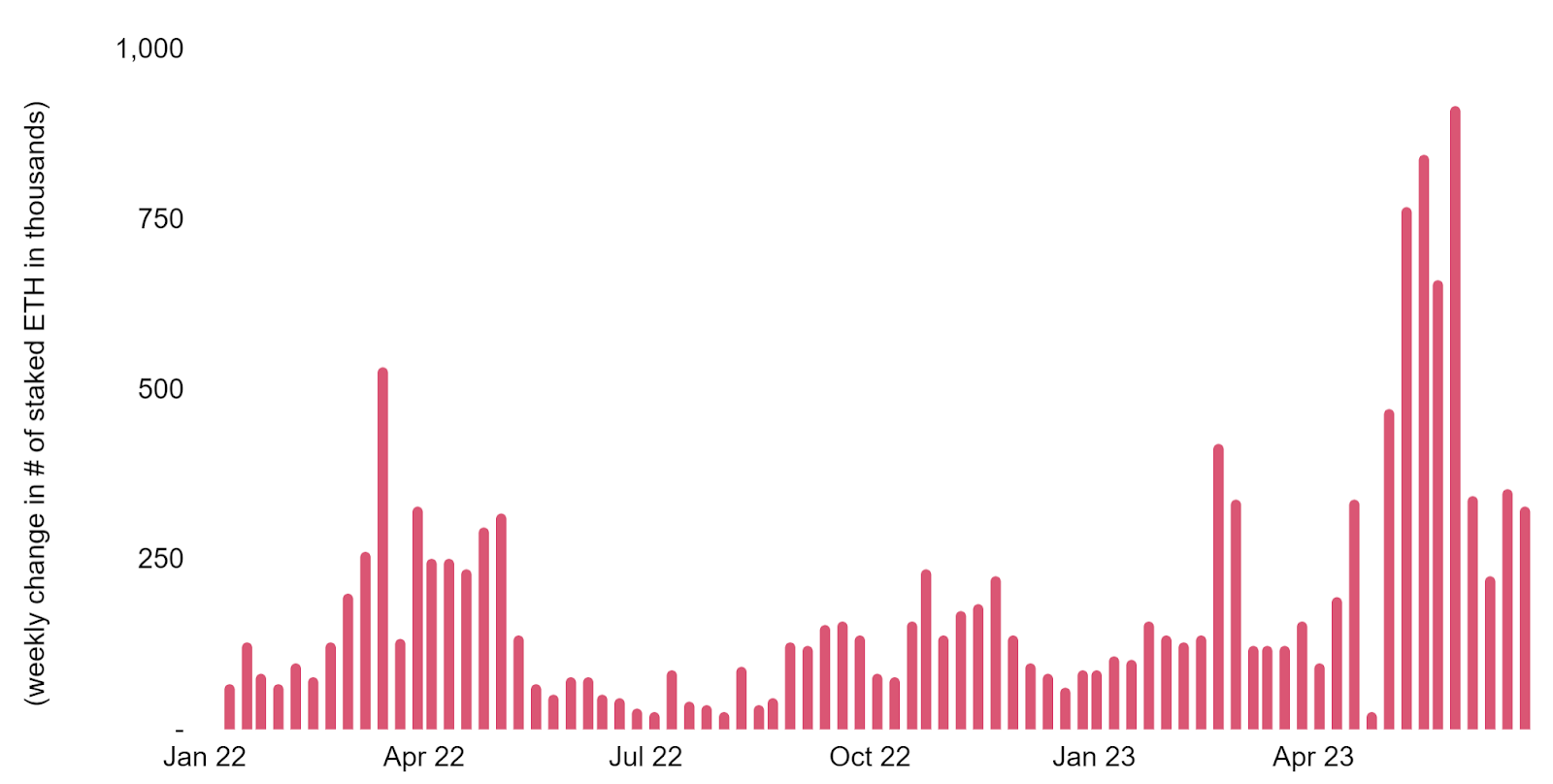

Graph I - ETH staking deposits reached new highs after upgrade “Shapella”

On April 12th, Ethereum underwent a significant upgrade known as “Shapella”. This upgrade allowed validators to withdraw funds from the ETH staking contract, thereby reducing the risk previously perceived by stakers. Following this change, Ethereum saw a substantial increase in the share of ETH staked. At writing, Lido controls approximately 30% of the market share.

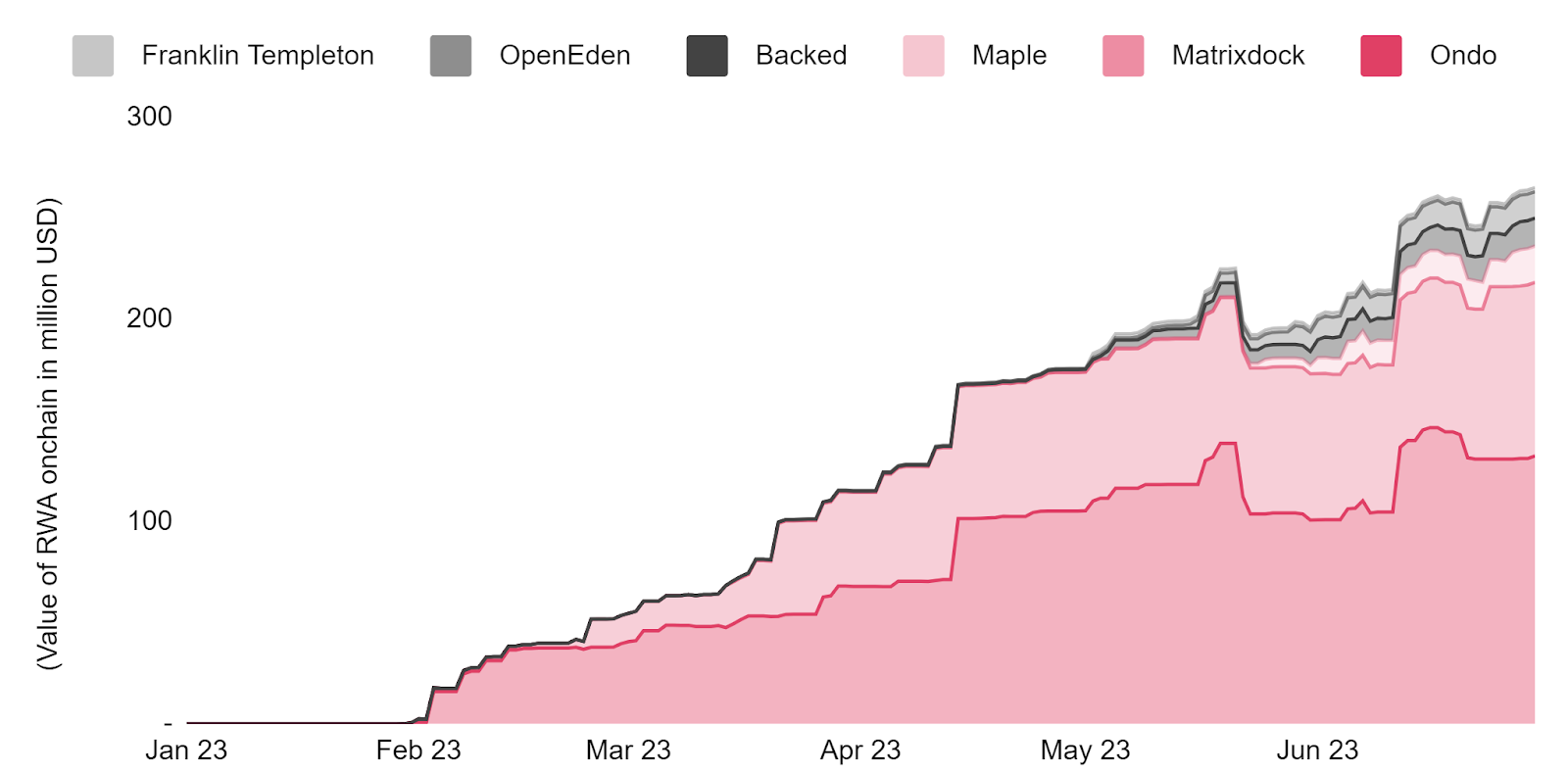

Graph II - Value of RWAs on-chain (excl. stablecoins) gained momentum

A number of protocols issuing RWAs on-chain have launched since the start of the year. These RWAs primarily include treasury bills and money market funds. In April, Maple launched their cash management pool, focusing on T-Bills and has since attracted approximately $20M in deposits.

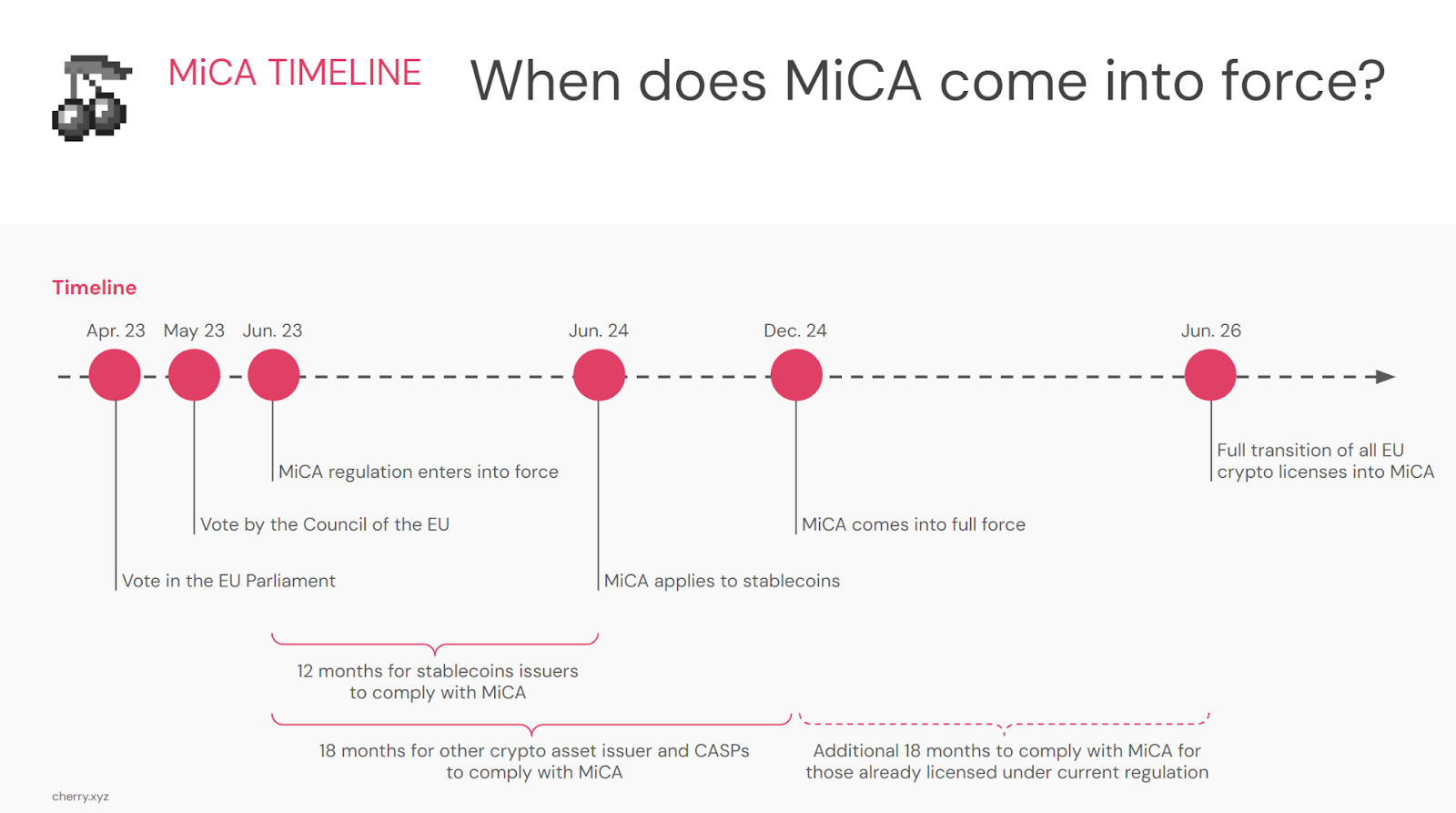

Graph III - MiCA regulation now in force in the EU

With MiCA, the EU created a comprehensive legal framework for crypto assets. The regulation has given the EU an opportunity to become a leader in defining legal certainty for both crypto companies and users, setting high standards similar to the regulation of other financial assets.