We recently shared this market update as part of our 1Q2024 update to our own investors. We’d like to share this context more broadly as it may be helpful to founders, LPs, VCs, and others elsewhere.

The first quarter of the year saw a continuation of the strengthening bullish sentiment across the industry. Public markets had a strong quarter with the cumulative market cap of crypto assets rising by 60% to reach $2.8T. Bitcoin experienced a significant milestone with the approval of the first spot Bitcoin ETF, which became the fastest growing ETF in history. Additionally, Bitcoin reached a new all time high of $73,737 on March 14.

In spite of the bullish sentiment, we are wary of the increasing frenzy in the market. Crypto is a very reflexive asset class, prone to rapid and extreme fluctuations. In spite of a series of positive developments for the industry, we feel that the level of excitement, and by extension prices, in both public and private markets are getting ahead of themselves.

Our investment strategy remains unchanged. We are continuing to invest consistently, though with increased caution given the current market conditions.

Bitcoin

After months of legal battles and anticipation, the SEC officially approved the first wave of spot Bitcoin ETFs at the beginning of January. While spot Bitcoin ETFs have been available in other markets, this is the first time US institutional and retail investors could gain direct exposure to Bitcoin through a regulated product. Prior to this, investors were confronted with either the risk and complexity of holding Bitcoin directly or the higher costs of the Bitcoin futures ETFs. The US regulatory body cleared 11 ETFs to list, with sponsors including Blackrock, Fidelity, Grayscale and Ark.

The inflows to the ETFs have since been substantial. Larry Fink revealed that the BlackRock spot Bitcoin ETF was the fastest growing ETF in history. By the end of April, the total holdings of the 10 spot Bitcoin ETFs with known Bitcoin addresses was 834k, which at the time equated to roughly $59.5B. The impact of the ETF along with the general bullish market sentiment pushed the BTC price to $71,247 at the end of the quarter, a 69% price increase from $42,208 at the beginning of the quarter.

In addition to the ETF developments and price action, Bitcoin is currently undergoing a renaissance, with increased interest and development activity around creating programmability layers and applications on top of Bitcoin. We’ve written more about what’s happening here.

At a high level, it’s historically been difficult to build on Bitcoin for a variety of reasons. However, recent technical unlocks have now made it easier for developers to do so. Bitcoin-based DeFi and NFT ecosystems are emerging, as well as a multitude of L2s, that promise to further widen the scope of what’s possible to build. While we don’t think that the breadth of applications will be as wide as what we see on other blockchains such as Ethereum and Solana, we think the opportunity to unlock crypto’s most valuable asset, BTC, is a compelling opportunity.

Base

In August of last year Coinbase launched its own Ethereum L2, Base. Like other L2s, Base improves the user experience by simultaneously increasing the speed and decreasing the cost of transactions by using Ethereum only to publish data while executing all computation off of Ethereum. Since Ethereum’s latest upgrade, Dencun, went live on March 13th, the median transaction cost on Base has dropped to less than half a cent. The aim of Base is to serve both as the home for Coinbase’s onchain products as well as foster an open platform for third party developers to build on.

The execution so far by the Base team has been phenomenal, reflected both in numbers and the new user behaviours emerging. Base’s total value locked (TVL) is up 167% over the quarter, increasing from $437.16m to $1.168B. While TVL is a useful and commonly cited metric that measures the amount of assets held within Base, what is perhaps even more interesting is the revenue Base is generating for its parent company Coinbase. Base generates fees by running a sequencer, which in the context of L2s are services that process and batch transactions together to then publish onto Ethereum. For providing this service, sequencers take a fee for each transaction. In Q1, the Base sequencer generated $27m in revenue, and at the time of writing, is operating at an annualised revenue run rate upwards of $250m.

The low fee environment, deep integration, and strong cross distribution with Coinbase’s existing products have made Base the destination of choice for the newest generation of crypto-enabled consumer products. What Base has also demonstrated is that centralised companies building on decentralised infrastructure can be big business.

Farcaster

Farcaster, the open source and decentralised social networking protocol, had a breakout quarter. As opposed to other centralised social networks, Farcaster is designed to expose its social graph to the open, which means that any third party developer can access that graph and build experiences on top of it. In the early days of Facebook and Twitter, both platforms allowed third party developers to build experiences that utilised their data and distribution. However, when it became clear that granting third party developers access ran counter to their own ad-based business models, both platforms ultimately cut off those developers. This is different on Farcaster, where developers have the assurance that no central party is able to deplatform them due to the protocol’s open source and decentralised design.

The Farcaster protocol can be accessed through around half a dozen clients. The most popular one at the moment is Warpcast, which is developed by the same core team behind the Farcaster protocol itself, but other popular clients include Supercast, Fiids, Yup, and Firefly which are all built by independent teams.

When users create a Farcaster account, they link a crypto wallet to that account. The pairing of a social account with a crypto wallet is a key point of differentiation between a web3 and web2 enabled social experience. Having a wallet embedded on Farcaster enables payments and the custody of digital assets directly within the social experience.

The trigger for Farcaster’s strong momentum this quarter was the launch of Frames, which enabled third party developers to build embedded applications that are compatible inside any Farcaster client. Through Frames, for example, users can purchase items from third party marketplaces directly on the Warpcast or Supercast UI instead of having to jump into another application or website.

While the absolute number of users on Farcaster cumulatively is still small, we’re seeing the ecosystem pick up momentum and will closely be following its development.

The quarter in 3 charts

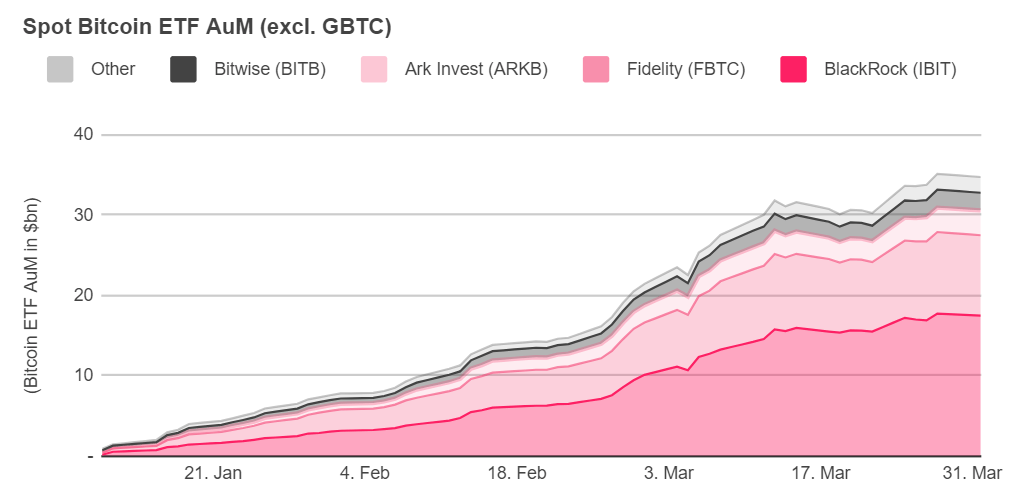

Green light for the Bitcoin ETF

In early January 2024, the SEC finally approved the launch of the first wave of Bitcoin spot ETFs, managed by key financial institutions such as BlackRock, Fidelity, and Ark Invest. Throughout the first quarter of 2024, the leading spot Bitcoin ETFs accumulated more than $35bn in AuM.

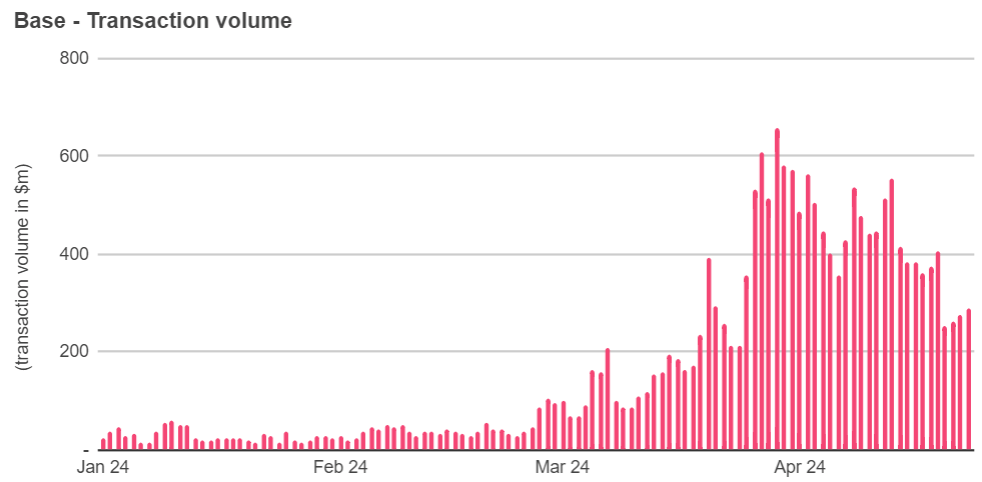

Base volume surges

Base set new records across all key metrics and currently processes over 2.2 million daily transactions, outpacing older alternatives such as Arbitrum and Optimism in network activity.

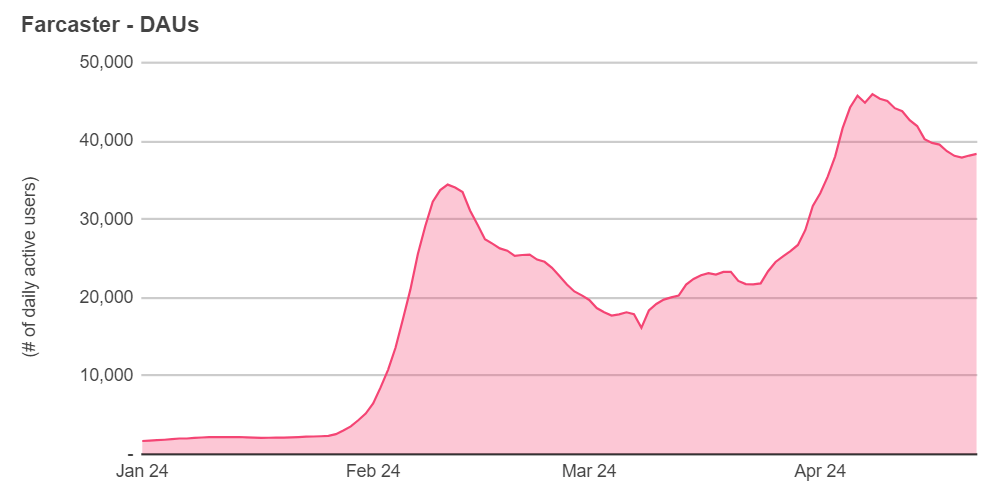

The rise of Farcaster

Since January, Farcaster has seen a significant increase in daily active users, with over 325k sign-ups and approximately 50k daily active users.